Solar isn’t just an energy solution anymore — it’s a powerful business investment. But for most companies, the biggest question isn’t whether to go solar; it’s how to pay for it.

Choosing the right Commercial Solar Financing structure can significantly affect your upfront costs, long-term savings, tax benefits, and ownership value. The right choice will depend on your organization’s financial goals, tax position, and appetite for long-term returns.

In this detailed guide, we’ll break down the three main options for Commercial Solar Financing — Power Purchase Agreements (PPA), Leases, and Cash Purchases — and help you decide which fits your business best.

At Colite Technologies, we’ve helped countless organizations across the Southeast navigate these choices to achieve the best balance between performance, profitability, and flexibility.

Why Choosing the Right Commercial Solar Financing Model Matters

Every business is different. A manufacturer might prioritize ownership and depreciation benefits, while a nonprofit might prefer predictable monthly payments with no upfront costs.

Your Commercial Solar Financing decision will shape your:

- Initial investment requirements

- Monthly cash flow

- Eligibility for tax incentives and depreciation

- Total long-term commercial solar savings

Let’s take a closer look at how each option — PPA, Lease, and Cash Purchase — impacts those outcomes.

Understanding Commercial Solar Financing Basics

Before diving into comparisons, it’s helpful to understand what Commercial Solar Financing really means. In simple terms, it refers to how a business funds its solar installation — whether by paying upfront, borrowing, or entering into an agreement to buy power over time.

Three popular approaches dominate the market:

- Power Purchase Agreement (PPA): You pay for the power, not the panels.

- Solar Lease: You pay a fixed monthly fee for system use.

- Cash Purchase: You buy and own the system outright.

Each model affects ownership, savings, and financial returns differently.

1. Power Purchase Agreement (PPA)

A Power Purchase Agreement (PPA) is one of the most popular Commercial Solar Financing options for businesses that want to benefit from solar energy without investing upfront capital.

How It Works

Under a PPA, a third-party investor (the system owner) installs and maintains the solar panels on your property. Your business simply buys the electricity generated — typically at a lower rate than your current utility cost.

You pay for energy, not equipment.

Key Benefits

- No Upfront Cost: The developer covers all installation expenses.

- Instant Savings: Electricity rates are often 10–30% lower than utility rates.

- No Maintenance Worries: The provider handles upkeep and performance monitoring.

- Predictable Energy Costs: Fixed or gradually escalating rates provide long-term stability.

Considerations

- You don’t own the system.

- You can’t claim tax credits or depreciation.

- Total lifetime savings may be lower than a cash purchase.

Best For

Organizations that want immediate savings with zero upfront investment — especially schools, municipalities, or businesses that prefer operating expenses (OPEX) over capital expenses (CAPEX).

PPA structures are widely available across states like South Carolina, Georgia, and Virginia, where supportive legislation enables third-party ownership models.

2. Solar Lease

A solar lease is similar to a PPA but structured slightly differently. Instead of buying the power, you pay a fixed monthly lease payment for use of the solar system installed on your property.

How It Works

The installer or financing company retains system ownership and maintenance responsibilities. You pay a set monthly fee — not tied to energy production — for the right to use the system.

Key Benefits

- No Capital Outlay: Like a PPA, there’s little to no upfront cost.

- Fixed Monthly Payments: Easier to budget than fluctuating utility bills.

- Maintenance Included: The leasing company keeps the system running efficiently.

- Shorter Contracts: Lease terms usually run 10–15 years.

Considerations

- You don’t benefit from tax incentives or depreciation.

- Payments remain fixed, even if energy production varies.

- You might save less long-term compared to a cash purchase.

Best For

Businesses that want stable payments, predictable budgets, and a hands-off approach. Leases can also be a bridge to ownership through buyout options at the end of the term.

Understanding PPA vs Lease dynamics helps clarify your path — both deliver short-term savings, but leases provide more predictable payments, while PPAs tie costs to actual energy use.

3. Cash Purchase

Paying cash upfront remains the most direct and financially rewarding Commercial Solar Financing method for businesses with available capital.

How It Works

You pay for the system in full, take ownership immediately, and enjoy all financial incentives — including tax credits, depreciation, and full energy savings.

Key Benefits

- Maximum Long-Term Savings: You eliminate monthly payments entirely.

- Full Ownership: Your business owns all energy generated and retains any excess value.

- Tax Advantages: Claim the 30% Federal Investment Tax Credit (ITC) plus accelerated depreciation.

- Higher Asset Value: Solar adds tangible value to your property.

Considerations

- Requires significant upfront investment.

- Payback typically takes 4–7 years.

- You’re responsible for system maintenance (though costs are minimal).

Best For

Companies seeking the highest commercial solar savings and ROI, especially those with strong tax liabilities to offset.

Cash purchase options also work well for organizations investing in long-term sustainability infrastructure, as systems can last 25+ years with minimal maintenance.

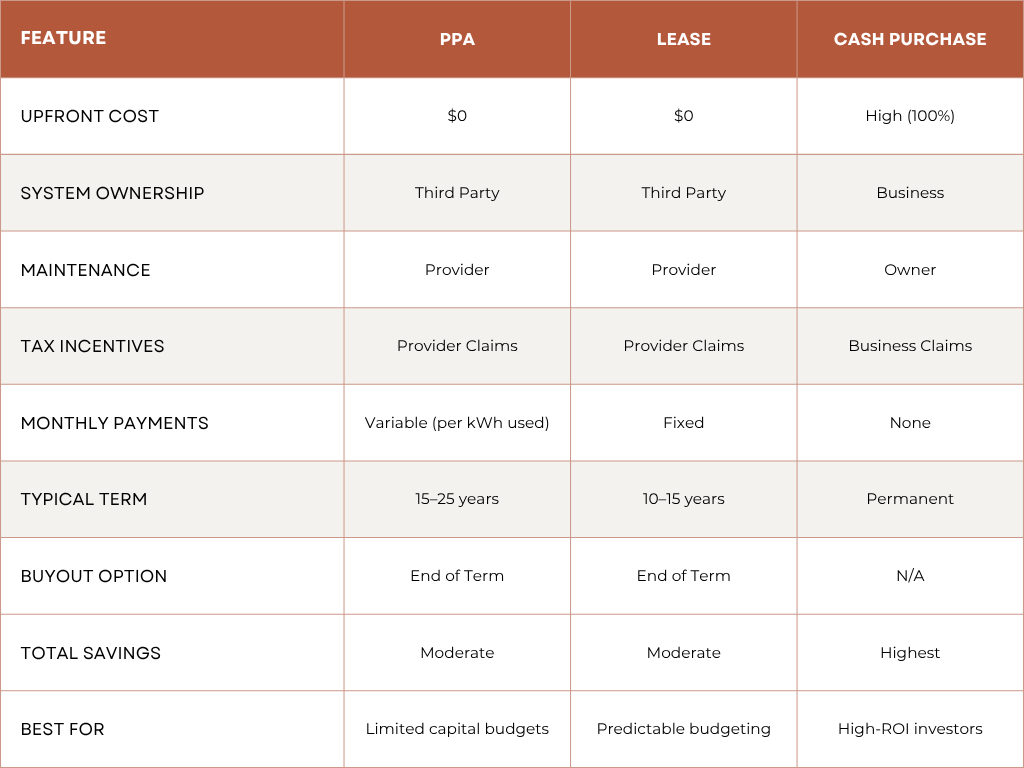

Comparing PPA, Lease, and Cash Purchase

To make your solar investment comparison easier, here’s a side-by-side overview:

Each Commercial Solar Financing option comes with its strengths. The right choice depends on whether you value immediate savings or long-term ownership returns.

Tax Incentives and Depreciation Benefits

Tax credits and depreciation are powerful tools in Commercial Solar Financing.

- Investment Tax Credit (ITC): Currently provides a 30% credit on total system cost.

- MACRS Depreciation: Allows businesses to recover investment costs through accelerated deductions.

These incentives can dramatically improve payback periods and overall returns — but only if you own the system through a cash purchase or financed ownership structure.

For businesses in regions like South Carolina, Georgia, and Virginia, local programs may add further rebates or performance-based incentives that enhance your commercial solar savings.

Commercial Solar Financing and ROI

No matter which model you choose, the goal is strong financial performance. A well-designed Commercial Solar Financing plan ensures:

- A short payback period (typically 4–8 years).

- Long-term cost predictability.

- Energy savings that exceed financing costs.

With energy rates rising nationwide, the value of these savings compounds over time — even modest reductions in monthly bills can translate to hundreds of thousands in long-term profit.

At Colite Technologies, our financial modeling tools help businesses visualize their solar ROI based on installation costs, incentives, and local energy prices.

Common Mistakes When Choosing a Financing Option

Even with multiple Commercial Solar Financing models available, many companies make costly missteps that delay or reduce ROI.

Avoid these common pitfalls:

- Ignoring Tax Eligibility: Not every organization qualifies for the same incentives.

- Overestimating Production: Always use verified energy modeling data.

- Choosing Based on Short-Term Cost Only: Lower upfront costs don’t always equal higher lifetime value.

- Neglecting Maintenance Terms: Ensure ongoing service responsibilities are clearly defined.

- Failing to Compare PPA vs Lease Accurately: Understand long-term cost differences before signing.

Working with experienced solar partners ensures your financing model aligns with your business goals and risk profile.

The Role of Business Solar Financing in 2025 and Beyond

The solar finance landscape continues to evolve. In 2025, businesses have access to more business solar financing products than ever before, including green loans, sustainability bonds, and ESG-linked investments.

Emerging trends include:

- Flexible financing structures combining PPA and loan elements.

- Performance-based agreements that link payments to verified energy production.

- Sustainability reporting integration, aligning solar investments with corporate ESG goals.

As markets mature, the line between finance and sustainability is blurring — and businesses that act early on these opportunities will gain a competitive edge.

How to Choose the Right Commercial Solar Financing Plan

When deciding between PPA vs Lease vs Cash Purchase, consider:

- Your Financial Objectives

- Looking for immediate savings? → Choose a PPA.

- Need predictable payments? → Choose a Lease.

- Want the best long-term ROI? → Choose Cash Purchase.

- Your Tax Position

- If you can utilize tax credits and depreciation, ownership models (cash or financed) are ideal.

- Your Capital Availability

- PPAs and Leases require no upfront cost — perfect for businesses preserving liquidity.

- Your Long-Term Plans

- Businesses with stable locations benefit most from ownership.

- Tenants or short-term occupants might prefer flexible PPAs.

- Your Sustainability Goals

- All models reduce emissions and operating costs, but ownership showcases a stronger environmental commitment.

Regional Opportunities for Commercial Solar Financing

The Southeast U.S. is emerging as one of the most promising solar markets for businesses.

- South Carolina: Offers property tax exemptions and energy rebates for commercial installations.

- Georgia: Boasts low installation costs and utility partnerships supporting large-scale adoption.

- Virginia: Features strong net metering policies and corporate solar incentives.

No matter where you operate, Commercial Solar Financing can be tailored to fit state-specific programs for maximum return. Learn more about available incentives through Colite Technologies’ South Carolina, Georgia, and Virginia pages.

Case Example: Comparing the Three Options

Let’s illustrate how each Commercial Solar Financing option performs for a mid-sized business in South Carolina installing a 250 kW system.

While the cash purchase solar option delivers the highest ROI, many businesses start with PPAs or leases to minimize risk and preserve capital — and later transition to ownership once they see proven results.

Final Thoughts: Powering Profitable Growth Through Smart Financing

The right Commercial Solar Financing plan can transform your energy expenses into long-term assets. Whether you choose a PPA, lease, or cash purchase, the key is aligning your financial strategy with your business goals.

At Colite Technologies, we help businesses evaluate financing options, secure incentives, and design high-performance systems that maximize both savings and sustainability.

Serving companies across South Carolina, Georgia, and Virginia, we simplify every step of your solar investment journey — from feasibility to installation and ongoing optimization.

Ready to compare your options and discover your best path to energy independence? Visit Colite Technologies today to schedule a free consultation and start unlocking the power of smarter financing.